Car Insurance Discounts 2026: How to Stack Your Way to a Lower Premium

What are the best car insurance discounts in 2026? The most impactful discounts in 2026 are Telematics/Usage-Based programs (saving up to 30%), Multi-policy bundling (saving 10–25%), and Full-payment rebates (saving 5–15%). Additionally, drivers of newer vehicles with Advanced Driver Assistance Systems (ADAS) or Electric Vehicles (EVs) can see further reductions of 10% or more as insurers reward safer, greener tech.

The “Big Three” Lifestyle Discounts

These remain the heavy hitters for most households:

-

The Bundle (Multi-Policy): Still the king. Combining home and auto can save you an average of $900–$1,000 per year.

-

Telematics (UBI): If you’re a safe driver, programs like State Farm’s Drive Safe & Save or Liberty Mutual’s RightTrack are offering up to 30% off for smooth braking and consistent habits.

-

Loyalty vs. The “Switch” Discount: While some carriers offer a 3-5% loyalty bonus, many now offer a 10% “Early Bird” or “Switch” discount for signing your new policy at least 7 days before your old one expires.

If you’ve renewed your car insurance lately, you probably felt the pinch. Prices keep climbing and fast. According to the National Association of Insurance Commissioners (NAIC), the average American paid 14.4% more for auto coverage in 2023 alone.

But here’s the good news: there’s a quiet way to fight back that is car insurance discounts.

They aren’t flashy. You won’t see ads for them every day. Yet for many drivers, they can shave hundreds of dollars off annual premiums without touching coverage levels. So, if you’re wondering how to pay less while keeping your protection intact, this guide will walk you through every meaningful discount, how to qualify, and what smart drivers are doing differently in 2025.

The Real Story Behind Car Insurance Discounts

Most people assume car insurance prices are set in stone. But insurers actually personalize rates using dozens of variables like your driving history, location, type of vehicle, mileage, and even how you pay.

Discounts are how they reward low-risk behavior. A clean driving record? That’s less of a risk. Owning multiple policies? That’s loyalty. Drive less or drive safer? That’s data-backed proof you’re a good bet. Understanding these small price breaks and how to stack them can help you save anywhere from 10% to 40% on your premiums depending on your profile.

Why 2026 Is the Year to Rethink Your Discounts

After a few volatile years in the insurance industry, 2026 is shaping up to be the year of smart shopping. Insurers are competing hard for loyal, low-risk customers, which means new programs and better incentives are emerging. For instance, Progressive’s Snapshot program now averages about $322 in savings per year for good drivers, while companies like State Farm and GEICO are offering up to 23% off for bundling multiple policies (Forbes).

The key takeaway? The best car insurance discounts aren’t hidden, they’re just underused.

How Discounts Affect What You Pay

Before diving into specific discounts, it helps to understand how insurance pricing works:

- Your premium depends on your driving record, claim history, location, vehicle type, credit (where allowed), coverage limits & deductibles.

- Discounts reduce your premium or sometimes offer bonus perks (like vanishing deductibles) but often come with eligibility rules.

- Discount stacking lets you combine several discounts: multi-policy + safe driver + multi-car, etc. but insurers often limit how many you can combine, or how much total discount you can get.

Knowing these basics ensures you don’t chase rare discounts and better use the ones you already qualify for.

Most Powerful Car Insurance Discounts & Real Savings

Here are discount types that deliver big savings, with real numbers and examples. If you qualify for just a few, you can easily save hundreds per year.

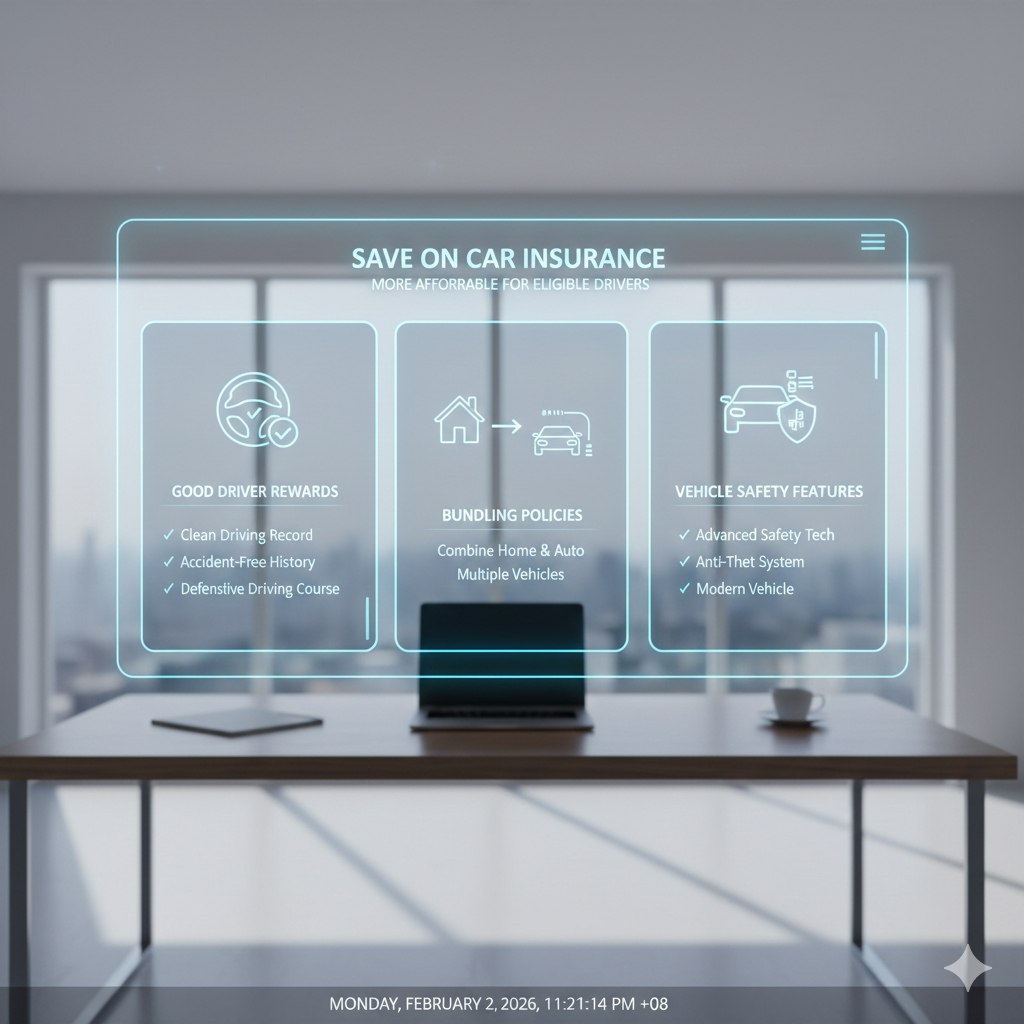

1. The Power of Bundling

- Bundling or combining home, renters, and auto insurance under one provider is one of the easiest ways to save. According to Forbes Advisor, the average driver who bundles saves around 14%, but some major insurers offer up to 23% off total premiums.

- Think of it like buying wholesale: insurers reduce your cost because you’re giving them more business and simplifying their risk management.

2. Safe Driver Rewards

- If you’ve kept a clean record for a few years with no accidents, tickets, or claims your insurer probably already owes you a discount. Companies typically reduce premiums by 10–30% for accident-free periods of 3–5 years.

- Add in modern telematics programs that track safe driving habits via smartphone apps or car sensors, and your savings can increase even further. Progressive Snapshot users, for example, save an average of $322 annually, though drivers with risky patterns may see smaller returns.

3. Student and Family Discounts

- Got a young driver on your policy? Then you know how expensive it gets. Fortunately, most insurers offer good student discounts (usually for GPAs above 3.0).

The Forbes 2025 report found these typically range between 10% and 18%.

If your teen or college student maintains good grades, that’s an easy way to offset the cost of being a new driver.

4. Drive Less, Pay Less

- If you only drive occasionally, say under 8,000–10,000 miles a year you could be leaving money on the table. Many insurers offer low-mileage or pay-per-mile plans that charge based on how often you drive.

According to data cited by Bankrate, drivers who keep annual mileage low save an average of $150–$300 per year. - With remote work becoming the norm, this discount is one of the most overlooked opportunities in 2025.

5. Safety & Anti-Theft Features

- Your car’s built-in tech can also save you money.

Modern vehicles with airbags, automatic braking, lane-assist systems, and anti-theft devices often qualify for 3–15% lower premiums.

Electric and hybrid vehicles are increasingly included too, with 5–10% eco-vehicle discounts being introduced across major insurers. - These might sound small individually, but stack two or three together and you could easily cross the 20% savings mark.

6. Deductible Rewards & Loyalty Programs

- Some insurers offer a vanishing deductible or deductible rewards: every year you avoid a claim, your deductible drops a bit, sometimes by $50-$100/year.

- Loyalty discounts (being a policyholder for multiple years) also bring savings. Combine these with safe-driver and policy payments (paid-in-full) discounts, and the savings add up.

How Real Drivers Are Saving

To put it in perspective, let’s imagine this:

Jane, a 30-year-old driver in Ohio, bundles her car and home insurance, drives safely, and uses a telematics app. Her insurer rewards her for good behavior.

- Multi-policy savings: 14% (~$280 off)

- Safe-driver program: 10% (~$200 off)

- Telematics reward: $322

Total annual savings? Nearly $800 that’s a full month’s rent or a plane ticket to Europe. That’s not just a lucky case. According to the Insurance Information Institute (III), the average U.S. driver can save between 25% and 35% by combining common discount programs and maintaining a clean record.

Regional Differences & Rising Rates

Your location plays a huge role in what you pay — and what discounts are available.

For instance, Texas drivers paid an average of $2,712 for full coverage in 2024, up 15% from the year before, according to the Houston Chronicle.

Meanwhile, drivers in states with lower accident rates and more competitive markets like Maine or Vermont can see much lower premiums and richer discount opportunities.

TIP: Always check your state’s rules and insurer options before assuming what’s “average.”

How to Qualify & Claim These Discounts

Knowing what discounts exist is great but you have to qualify and ask for them. Good news: many people leave money on the table simply because they don’t apply.

Here are proven strategies:

- Review your policy annually: life changes (new car, moved location, driver aging or graduating, etc.) might make you eligible for new discounts.

- Ask your insurer directly about each discount type: multi-policy, safe-driver, telematics, students, low mileage. Don’t assume they apply automatically.

- Install safety devices and maintain them: anti-theft alarm, tracking devices, fresh safety inspections.

- Drive safely: avoid tickets, at-fault accidents. Some states/insurers also reward defensive driving course completion.

- Choose your coverage smartly: sometimes matching a higher deductible or dropping rarely used coverage (if safe to do so) allows you access to other discounts.

A Few Cautions Worth Knowing

Not all discounts last forever. Telematics programs can raise premiums for risky driving. Some bundling offers expire when policies renew or after a claim. And state laws limit which discounts apply to which coverages. That’s why it’s worth reviewing your plan annually and comparing quotes then insurers adjust criteria constantly.

Decision-Time Checklist

If you want a concrete action plan, here are steps to use right away:

| Step | Action |

| A | Pull up your current car-insurance policy and list out: your premium, claims history, how many cars you insure, whether you bundle, etc. |

| B | Use tools or quote engines to compare what other insurers offer in your state (including bundling / telematics programs). |

| C | Contact your insurer & ask: “Which discounts do I currently have?” + “Which ones am I missing?” |

| D | Make small upgrades that cost little but can get discounts (safety devices, anti-theft alarm, drive fewer miles). |

| E | Re-evaluate every renewal period or after major life changes (finished school, new car, moving, etc.). |

Conclusion

Insurance discounts aren’t gimmicks. They’re rewards for responsibility for being a safe driver, loyal customer, and thoughtful policyholder. Even a 10% cut can mean $200–$400 saved every year, which adds up fast. Stack the right ones bundling, safe driving, low mileage and you could easily reduce your bill by a third without giving up full coverage.

Use the data above, talk to your insurer, compare quotes, and keep your driving record clean. Those are the simple but powerful levers that can help you keep more money in your pocket without giving up protection. So the next time you renew, don’t just click “auto-renew.” Pick up the phone. Ask about new car insurance discounts. Your wallet will thank you.

-

Need more info read this too “Best Time to Get Insurance“ post “The ‘Early Bird’ discount requires shopping at least 21 days before your renewal date.”

FAQs

Which insurance company offers the most discounts?

There’s no single “best” across all states, because discount offerings vary regionally. Companies like Allstate and Geico are known for offering a wide range of discounts (safety, loyalty, bundling) and publicizing them openly. (See Allstate’s discount page) Allstate

Who is cheaper, GEICO or Progressive?

On average, GEICO tends to offer more competitive rates for standard drivers, especially for minimum and full coverage options. In comparison, GEICO often comes out slightly cheaper than Progressive in many markets. Insurify+2NerdWallet+2

Who normally has the cheapest car insurance?

It depends heavily on your location, driving record, and vehicle, but in many U.S. states, GEICO, State Farm, or USAA (for eligible members) often appear among the lowest. In California, for example, GEICO had the cheapest full coverage average in recent analyses. NerdWallet

Is AAA insurance cheaper than Progressive?

In many cases, NO, Progressive tends to have lower average rates than AAA, though it depends on your state and coverage. One comparison showed AAA’s rate is about $108/month versus Progressive’s $113/month on average. The Zebra

Who has the best car insurance in California?

“Best” depends on priorities (price, service, coverage). But from a cost standpoint, GEICO is often ranked as one of the cheapest for full coverage in California lately. NerdWallet

How to get the best deal on car insurance?

Compare quotes from multiple companies in your state, then ask insurers directly about every discount you qualify for (bundling, safe driver, low mileage). Also maintain a clean driving record and install safety or anti-theft features these small changes often unlock the biggest savings.

Note: The content published on this blog is intended solely for informational and guidance purposes. We do not offer, promote, or provide any services through this website.