Compare Car Insurance Quotes: How to Beat the 2026 Rate Hikes

What is the best way to compare car insurance quotes in 2026? To get an accurate comparison, you must use a “Like-for-Like” strategy: ensure every quote has identical deductibles, liability limits, and add-ons. In 2026, the average cost for full coverage is $208/month, but you can save up to $800/year by comparing at least three providers and opting into Telematics programs (like State Farm’s Drive Safe & Save or Geico’s Drive Easy), which offer discounts for safe driving behavior tracked via your smartphone.

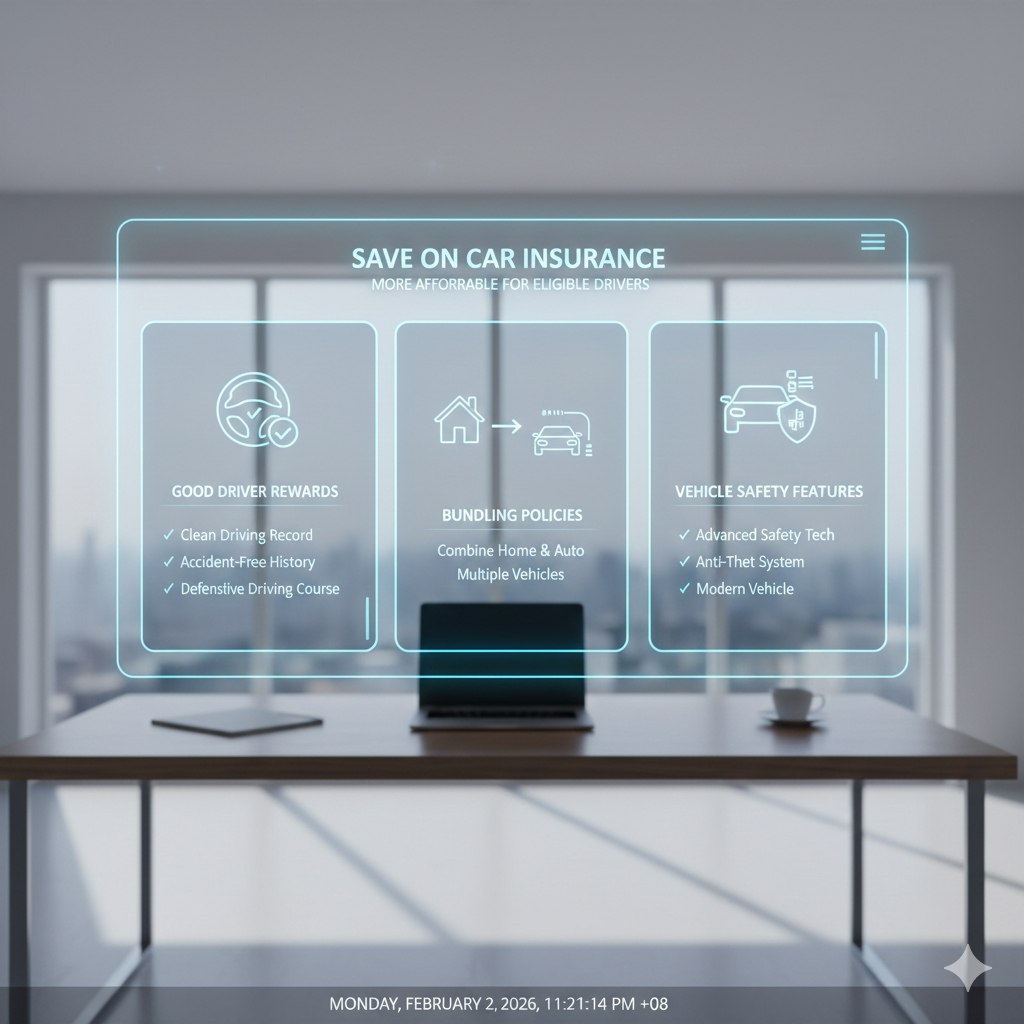

The “Big Three” Factors Affecting Your 2026 Quote

-

Vehicle Tech (ADAS): Sensors in your bumper and windshield make repairs 20–30% more expensive. If your car has autonomous braking, ensure the insurer recognizes these safety features for a discount.

-

Credit-Based Insurance Scores: In most states, your credit score is now a primary driver of your rate. Improving your score can save you more than a clean driving record in some regions.

-

Geography & Climate: If you live in a “High-Risk” ZIP code (prone to floods or high theft), your base premium will be higher regardless of your driving history.

If you’ve ever renewed your car insurance and felt your premium jump overnight, you’re not alone. In 2024, the average cost of car insurance across the U.S. rose by nearly 11%, marking the steepest increase in more than a decade (Bureau of Labor Statistics, 2024). At the same time, nearly *half of all drivers 49% are shopping for new insurance policies this year (J.D. Power U.S. Insurance Shopping Study, 2024). These numbers tell a story: drivers are no longer sticking with the same insurer year after year. They’re comparing, switching, and saving. But comparing car insurance quotes isn’t just about finding the cheapest rate, it’s about finding the right coverage at the right value.

This guide will walk you through how to compare car insurance quotes effectively, understand what really affects your rate, and know when it’s time to switch. Let’s get started.

What is a car insurance quote?

A car insurance quote is an estimate of the price for your insurance. This estimate is calculated using the answers you provide when you get your quote. It is not necessarily your final premium. Quotes are helpful because they give you an overview of what you can expect to pay based on the coverages you select. They give you an idea of what you’ll pay for an auto insurance policy from each carrier you get a quote from before committing to one. These quotes might all come out to different car insurance rates based on how risky each insurer considers the cars and drivers on your policy to be.

Why Comparing Car Insurance Quotes Matters

Most people renew their policy out of habit. But car insurance premiums are not static; companies adjust them regularly based on your driving record, ZIP code, vehicle, and even your credit score. Even if nothing has changed in your life, the market has changed around you. Insurers update their risk algorithms every few months, meaning two companies can now price your coverage hundreds of dollars apart for the same protection.

According to Insurify’s 2024 Rate Comparison Study, quotes can vary by 200–400% between the cheapest and most expensive insurers for the same driver profile. That’s the difference between paying $80 or $320 per month for identical coverage.

Before you start comparing, it helps to understand the basic types of car insurance coverage like liability, collision, and comprehensive. You can explore these in more detail on our Types of Car Insurance page.

How Car Insurance Quotes Actually Work

When you request a car insurance quote, you’re essentially asking an insurer: “How risky do you think I am?” Each company uses its own data model to answer that question.

A quote reflects more than just your driving record. It’s built on your:

- Coverage limits (how much your policy will pay per claim)

- Deductible (what you pay out of pocket before insurance kicks in)

- Personal profile (age, gender, marital status)

- Vehicle details (make, model, year, safety features)

- Driving history and credit-based insurance score

That’s why your friend in another ZIP code might pay half your premium even with the same car and clean record. The key to getting an accurate comparison is to make it “apples-to-apples.” That means comparing the same coverage limits and deductibles across all insurers. Otherwise, you might think one quote is cheaper when, in reality, it simply covers less.

Factors That Affect Car Insurance Quotes

Now let’s break down the factors that most influence your car insurance cost.

1. Driving Record

A single speeding ticket can raise your premium by 10–20%. Multiple violations can double it. Safe driving remains one of the strongest ways to qualify for discounts.

2. Age and Experience

Young drivers, especially those under 25, face the highest premiums. According to The Zebra’s 2024 State of Auto Insurance Report, drivers under 25 pay 2–3× more than older, more experienced drivers.

3. Location

Where you live matters. Urban areas with higher traffic and accident rates tend to have higher premiums than rural ones.

4. Credit Score

In most states, insurers use your credit-based insurance score to predict risk. Drivers with good credit can pay up to 24% less for identical coverage (Experian Auto Insurance Report, 2024).

5. Coverage and Deductibles

Opting for a lower deductible (like $250 instead of $1,000) increases your premium but reduces your financial burden if you file a claim.

6. Discounts and Bundles

Bundling policies like home and auto or maintaining a clean driving history can earn substantial discounts. Explore our guide on insurance discounts to find out how to lower your premium.

How to Compare Car Insurance Quotes the Right Way

Comparing car insurance quotes effectively isn’t about getting the lowest number, it’s about finding the best value for your situation.

Follow this step-by-step process to make sure you’re getting a fair comparison:

Step 1: Decide on Your Coverage First

Before you even start comparing, decide what coverage you actually need. Full coverage, liability-only, or a mix? Refer to our Car Insurance Basics page for clarity.

Step 2: Gather Consistent Information

Make sure all your quotes use the same details—vehicle, mileage, driver info, and coverage levels. Changing even one variable can skew results.

Step 3: Use Trusted Comparison Tools

Sites like Impurify, NerdWallet, or The Zebra allow you to view multiple quotes in one place. Just make sure the site provides real quotes and not just lead generation forms.

Step 4: Watch for Hidden Fees and Deductibles

Some “cheap” quotes hide higher deductibles or exclude key coverages like uninsured motorist protection.

Step 5: Read Customer Reviews

Price matters, but so does service. Look for customer satisfaction scores from J.D. Power or AM Best financial ratings.

A real example: A Florida driver compared quotes across three platforms and discovered a $740 annual difference for identical coverage (Insurify, 2024).

When’s the Best Time to Compare or Switch Insurers

Timing can play a big role in how much you save.

According to Forbes Advisor (2024), the best time to shop for car insurance is 30–45 days before your policy renewal. You’ll have enough time to evaluate options without risking a lapse in coverage. Another great time to compare quotes is after major life events, such as:

- Buying a new car

- Getting married

- Moving to a new city or ZIP code

- Adding or removing drivers

- Improving your credit score

Consumer Reports’ 2024 survey found that drivers who switch policies after major life changes save an average of 15–20% annually.

Where to Compare Car Insurance Quotes

Let’s talk about where to actually compare quotes. There are three main ways:

1. Direct from Insurers

You can get quotes straight from individual companies like GEICO, State Farm, or Progressive. This gives you precise rates but requires more time.

2. Independent Agents

A local or online independent agent can compare multiple insurers for you and explain policy differences in plain English.

3. Online Comparison Tools

Modern tools like Insurify, NerdWallet, or The Zebra let you view multiple quotes instantly. These platforms are free, secure, and use verified insurer data not just marketing leads.

At techoreview, our goal isn’t to sell policies but to educate you so you can compare confidently. If you’d like to explore options, check out our car insurance comparison tool for real-time rates from reputable insurers.

Common Mistakes to Avoid When Comparing Quotes

Even savvy drivers make mistakes when comparing car insurance quotes. Avoid these pitfalls to ensure you’re getting a fair deal:

- Choosing only the cheapest option.

Nearly 40% of drivers pick the lowest quote without realizing their deductible doubled or their coverage limits dropped (J.D. Power Claims Satisfaction Study, 2023). - Not reviewing exclusions.

Some low-cost policies exclude roadside assistance or rental reimbursement benefits that can save you later. - Ignoring financial strength.

Always check your insurer’s financial stability rating (A or higher by AM Best). - Not checking state requirements.

Minimum liability laws vary by state. Make sure your quote meets your state’s coverage requirements.

Understanding how the claims process works before you buy can also save you stress later visit our claims guide for a complete walkthrough.

Real-Life Example: How Comparison Helped a Family Save

Meet the Parkers, a family from San Diego with two vehicles, a Honda Civic and a Toyota RAV4. They’d been with the same insurer for six years, paying $2,180 per year for full coverage. When they finally compared car insurance quotes online, they discovered a regional insurer offering the same coverage plus roadside assistance for $1,368/year, a savings of $812 annually. That’s not unusual. According to NerdWallet’s 2024 auto insurance analysis, the average U.S. driver can save up to $652 per year simply by shopping around and comparing quotes every 12 months.

It’s proof that informed comparison doesn’t just save money it can help you find stronger, more reliable coverage.

Compare Smart, Not Just Cheap

The cheapest car insurance quote isn’t always the best one. Real savings come from balancing affordability, reliability, and adequate protection.

Before you hit “Buy,” take a few minutes to compare quotes side by side, understand your coverage, and check the insurer’s reputation.

If you’re ready to take the next step, here’s how to get started:

- Learn the different types of car insurance coverage.

- Use our car insurance comparison tool for instant quotes.

- Discover how to save with discounts and bundles.

The smartest drivers aren’t the ones who spend less, they’re the ones who know what they’re paying for.

Read our this “18 Wheeler Accident Lawyers“ post “Commercial insurance limits for trucks are vastly different from personal car insurance; see our guide on 18-wheeler liability for more.

FAQs

What is the best site to compare car insurance quotes in the USA?

In the U.S., Insurify is widely considered one of the best. It pulls real-time quotes from over 100 insurers, doesn’t charge fees, and has very high customer satisfaction. Insurify+1. The Zebra is another strong option, offering side-by-side comparisons from top providers quickly and transparently. The Zebra

Which car insurance comparison website is best for U.S. drivers?

For most people, Insurify stands out because it blends ease of use, broad insurer coverage, and strong ratings (around 4.8/5). Insurify+2Insurify+2

If you value seeing many options fast and comparing extras (discounts, add-ons, bundling), The Zebra or Compare.com are solid picks. Compare.com+1

How much can I save by comparing multiple car insurance quotes in the U.S.?

If you shop around, Americans can often save $1,000 to $1,600 per year (especially if they have poor credit) by finding the lowest premium. ValuePenguin

Even for good drivers, comparisons can knock hundreds off annual premiums. ValuePenguin+1

What should I look for when comparing car insurance quotes?

Beyond price, check your deductibles, coverage levels (liability vs full), and optional add-ons. A cheaper quote may leave you exposed. WalletHub+1

Also review the insurer’s reputation, claims process, and available discounts (safe-driver, bundling, etc.) to ensure you get value, not just savings. WalletHub+1

Note: The content published on this blog is intended solely for informational and guidance purposes. We do not offer, promote, or provide any services through this website.