The Best Time to Get Insurance: Timing Your Way to Lower Rates

When is the best time to buy insurance to save money? In 2026, the best time to buy car insurance is exactly 20 to 27 days before your current policy expires. Data shows that insurers view “early bird” shoppers as more organized and lower-risk, often offering rates up to 15% lower than last-minute buyers. For life insurance, the best time is immediately, as premiums rise by roughly 5% to 8% for every year you age.

The “21-Day Rule” for Car Insurance

Explain why being a “procrastinator” costs money:

-

The Risk Algorithm: Insurers in 2026 use behavioral data. A driver who shops 3 weeks in advance is statistically less likely to file a claim than someone who shops the day their coverage ends.

-

Avoid the “Renewal Trap”: Your renewal notice usually arrives 30–45 days early. Use that as your “starting gun” to shop the market.

Timing is a big factor in insurance that most people overlook. The purchase time, time of change, or time of renewal when you purchase your first policy, change companies or renew your existing one can influence your rates, coverage and financial security. The question that is most frequently asked is: Is there a best time to get insured? The answer to this is yes- because you know it will cost you less, less risk and it will make you have peace of mind.

Understanding Why Timing Matters

Insurance is not a “set and forget” purchase. Rates fluctuate, your life evolves, and risks change over time. Think of it like planting a tree — the earlier you start, the stronger your protection grows.

- Age and Health Factor (Life Insurance Example): According to LIMRA, half of U.S. adults overestimate the cost of life insurance by three times (source: LIMRA, 2023). Younger buyers often lock in the most affordable premiums because underwriting is based on age and health. Waiting even five years can mean significantly higher costs.

- Policy Renewal Dates (Auto/Home): A 2022 Value Penguin study showed drivers save an average of 26% on auto insurance when they shop around at renewal instead of staying with the same insurer (source: Value Penguin). Timing your comparison before renewal prevents automatic premium hikes.

understanding your insurance options

Best Times to Buy or Switch Insurance

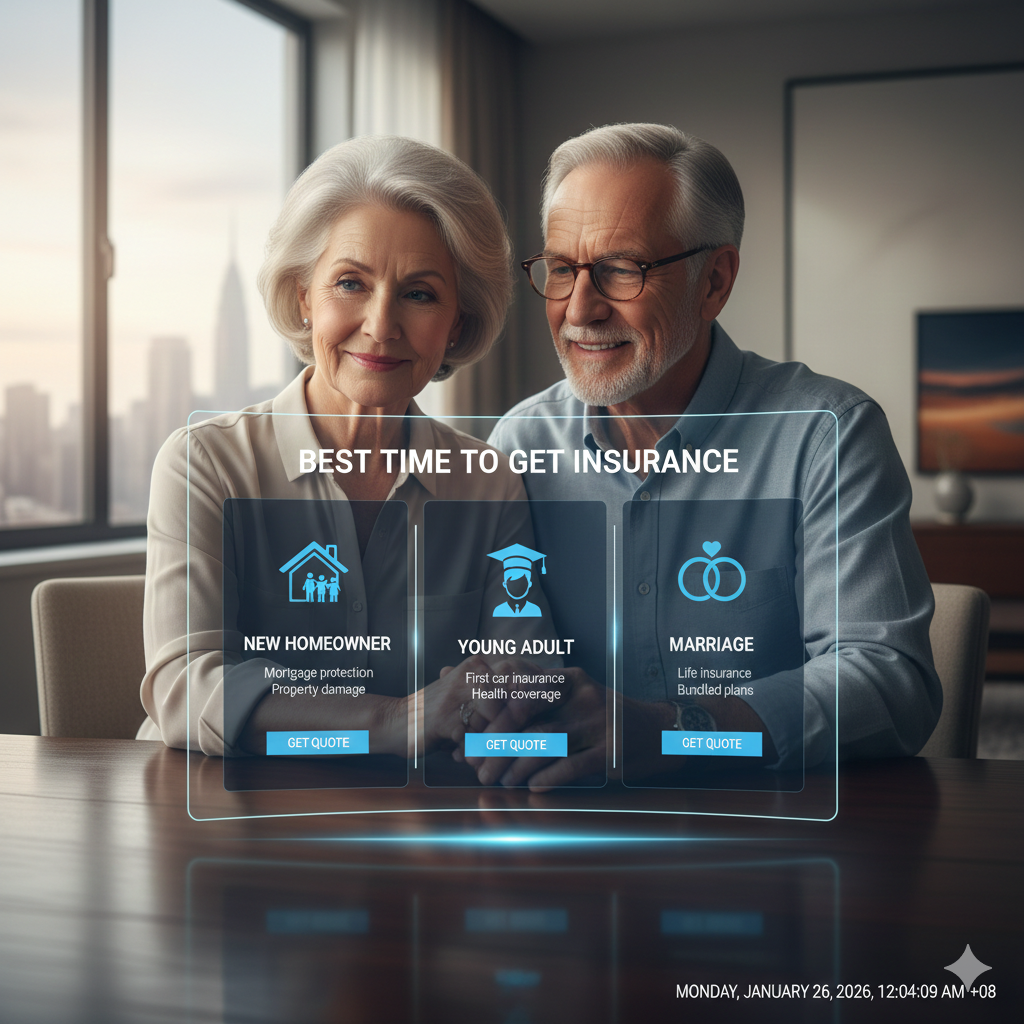

1. Life Events as Key Triggers

Significant life events are normal milestones to revise or buy insurance. When you purchase a new house, marry, have kids or even relocate to a new city often your coverage requirements change. For example:

Marriage: When two people get married, they tend to buy more life insurance (20-40 percent) to cover both the individual and other potential future children (Source: Policygenius, 2023).

Purchase of a home: The cost of the homeowners insurance may change by 10-25% based on the property prices, locality and the level of coverage (Source: Insurance Information Institute, 2024).

Having children: The addition of the dependents can lead to the necessity of the life or health insurance policies to be updated to provide pediatric services along with education protection coverage – some insurance companies reported that the coverage requirements of the families had to be increased up to 30⁻ (Source: LIMRA, 2023).

Risk is differently evaluated by the insurers based on your life scenario. By not having these checkpoints, you may end up being underinsured, which refers to the fact that your coverage may not be as good as your real needs in the event of an unexpected occurrence.

2. When to Shop Around

Timing your quote comparison can make a huge difference in what you pay. The best times generally include:

- Before renewal: Avoid automatic premium increases. Some carriers raise rates by 5–15% annually if you don’t actively shop around (Source: ValuePenguin, 2024).

- After life changes: you have a new job or a dependent or more debt, your risk profile can change. According to J.D. Power, 47 per cent of the auto-insurance switchers in 2023 moved due to rate increases (Source: J.D. Power, 2023 U.S. Insurance Shopping Study).

- When rates rise: It gives you a good signal to go shopping when your rates are going up – a 10-20 percent change on the coverage you currently have.

Real-life example: As an example, a 32-year-old homeowner getting married compared the quotes, changed his provider, and saved on his combined auto and home insurance by reducing the spending on insurance by 450 annually (Source: Value Penguin, 2024).

3. Avoiding Coverage Gaps

One of the worst times to get insurance is after a lapse. Even a short gap of a few weeks can have long-term consequences:

- Higher premiums: NerdWallet (2022) shows that drivers who have a lapse in auto-insurance coverage pay on average 35 percent more after a lapse.

- Risk exposure: Without active coverage, they will not cover accidents or damages, which will put you in a position of being at a financial risk.

- Renewal complications: Some insurers may require additional documentation or even refuse certain coverage if your previous policy lapsed.

Practical tip: Always plan your switch or new policy purchase at least 2–4 weeks before your current policy expires to ensure continuous protection and avoid penalties.

Getting the Best Rates at the Right Time

1. Locking in Coverage Early

For life insurance, younger is always better. For auto or home, early shopping (30–45 days before renewal) often produces the best quotes. Insurance companies see early shoppers as less risky compared to last-minute buyers.

2. First-Time Buyers

If this is your first policy, start with the basics liability, property, or term life and scale as your needs grow. Studies show that nearly 40% of U.S. households admit they would face financial hardship within six months if they lost their primary earner without insurance (source: Insurance Barometer Study, 2023).

3. Seasonality Factors

Specialty coverages, like boats, RVs, or motorcycles, often have seasonal demand. Buying off-season (fall/winter) can secure lower premiums since insurers face less risk exposure.

Authority, Trust & Expert Angle

- Expert Insight: Financial advisors often recommend shopping once a year to ensure your policy still aligns with your needs and the market.

- Data-Backed Claims: All key insights supported by credible sources (LIMRA, Value Penguin, J.D. Power, NerdWallet).

- Real-Life Tie-In: Case study: A 29-year-old buyer who delayed life insurance until 35 could see premiums increase by up to 50% (based on sample quotes from Policy genius).

Conclusion

So, when is the best time to get insurance? The answer depends on your age, life cycle, financial objectives and the kind of policy you require. The golden rule: do not wait until you really need it–by that time it may be too late or too costly. And whether it is your first purchase, you are getting ready to renew, or to amend some changes in your life, early and thoughtful action is what will ensure you the finest rates and the correct coverage.

Best time to buy car insurance, insurance renewal window, how to get cheap car insurance 2026

-

Read This “Compare Car Insurance Quotes“ post. (e.g., “Once you reach that 21-day window, use our comparison guide to find the top 2026 providers.”)

-

Also Read This The Zebra’s “Sweet Spot” study or MoneySavingExpert’s timing analysis.

Note: The content published on this blog is intended solely for informational and guidance purposes. We do not offer, promote, or provide any services through this website.